Call (844) NO-DISPUTES

Call (844) NO-DISPUTESHow to Write a Chargeback Rebuttal Letter That Wins

But most rebuttal letters fail before anyone even reads them. They're too long, emotional, or missing the exact evidence the bank needs to reverse its decision. Card networks and issuing banks follow strict laws, and if your response doesn't speak their language, it gets written off - regardless of whether you're right.

This guide will talk about how to write a chargeback rebuttal letter that actually works. You'll learn what to include, how to structure your argument, which evidence carries the most weight, and the mistakes that kill an otherwise strong case. Whether you're disputing your first chargeback or you've been through the process before, the goal here is simple: give you the tools to build a response that gets taken seriously.

What Banks Actually Look for in a Chargeback Rebuttal Letter

When a customer disputes a charge, the bank looking over your rebuttal isn't reading it the way a person would read a complaint letter - it runs the rebuttal against a checklist with something called a reason code - a short code that tells everyone involved why the dispute was filed. Every reason code has its own set of acceptable evidence, and if your rebuttal doesn't address that code, it gets set aside regardless of how well it's written.

That's worth sitting with for a bit. The bank isn't choosing who's telling the truth - it's choosing if you've submitted the right documentation to meet the threshold for that particular dispute type.

Issuers review rebuttals for two things above everything else: relevance and verifiability. Vague statements like "the customer received their order" don't move the needle. What does move the needle is a delivery confirmation with the cardholder's address, a signed receipt, or a timestamped record of communication. The more your evidence can be checked independently, the stronger your position.

Emotional replies get discarded faster too. A rebuttal that explains how much effort went into fulfilling an order, or how unfair the dispute feels, gives the reviewer nothing to work with. Banks need facts they can document in their system - not context they can't verify.

The submission window is also tighter than most merchants know. Depending on the card network, you usually have between 7 and 11 days to respond once a chargeback is initiated. That timeline includes the time it takes to collect your evidence, write your letter, and submit everything through the right channel. There's no room to scramble.

"Winning" a chargeback from the issuer's perspective means one thing: you've demonstrated, with documentation, that the original transaction was valid. That the customer's claim doesn't hold up against the evidence. The bar is whether your submission satisfies the requirements for that reason code and leaves the reviewer with no procedural reason to side with the cardholder.

This framing changes how you approach the whole process. You're not writing a defense - you're building a file.

Gathering the Right Evidence Before You Write a Word

Before you type a single sentence of your rebuttal, you'll have to pull together everything that supports your case - this step takes most merchants between one and three hours, which is quite a bit when you're already frustrated. But skipping it - or rushing through it - is the main reason merchants lose disputes they should have won.

But a lot of merchants submit whatever they can find fastest. An order confirmation here, a screenshot there. Banks see this all the time and it doesn't move the needle. You want to match your evidence to the claim being made against you.

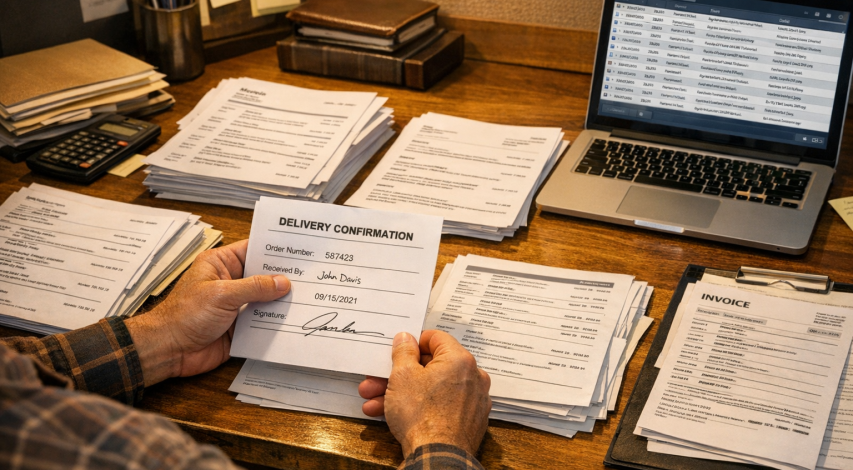

A signed delivery confirmation is one of the strongest pieces of evidence you can have for an "item not received" dispute - it directly contradicts the cardholder's claim and leaves very little room for argument. IP address and device logs are equally strong when the chargeback involves fraud or identity claims, because they can show that the actual account holder was the one who made the purchase.

Email threads and chat logs land in the middle ground. They help to show the relationship between you and the customer and can show that the product or service was received and accepted. They're harder to dismiss than nothing, but they don't carry the same weight as a physical signature or a login record with a known device.

An order confirmation on its own is weak - it proves a purchase happened but says nothing about delivery, use, or satisfaction. Treat it as a supporting document instead of your main argument. If you're dealing with a situation where a customer already received a partial refund before filing, understanding how that affects your case is worth doing before you write a word.

| Evidence Type | Best Used For | Strength |

|---|---|---|

| Signed delivery confirmation | Item not received claims | High |

| IP address / device logs | Friendly fraud / identity claims | High |

| Email or chat history | Service/product disputes | Medium |

| Order confirmation only | General proof of purchase | Low |

Go through your records and collect everything relevant before you choose what to include. Lead with your strongest evidence and use the rest to fill in the story around it.

How to Structure Your Rebuttal Letter Step by Step

Now that you have your evidence ready, it's time to put the letter together. A well-structured rebuttal takes one to two hours to write properly - and that time is worth spending - in friendly fraud cases, merchants with strong submissions win as much as 43% of the time.

The hardest part for most merchants is not the writing itself but the instinct to explain how frustrating the situation is. That emotional pull is understandable, but the bank looking over your letter doesn't weigh feelings - they weigh facts. You want to write like you're filing a report, not venting to a friend.

Start With a One-Paragraph Summary

Open with a quick, factual summary of your position. State who you are, what the transaction was, and what outcome you are requesting. Keep it to three or four sentences and write it in plain language. Think of it as giving the reviewer everything they need to know about your case before they read a single page of evidence.

Build a Factual Timeline

After your summary, list what happened in chronological order. Start from the date of purchase and move through fulfillment, delivery, and any customer communication. A simple numbered list works well here because it makes the sequence easy to scan. This part of the letter does the heavy lifting, so be precise with dates and limit each point to one fact.

Reference Your Evidence Directly

Attach your documents and point to each piece of evidence by name in the body of the letter. Something like "see attached delivery confirmation dated June 3rd" tells the reviewer where to look and keeps your argument grounded. Label your attachments to match what you reference in the letter.

Close With a Direct Request

End the letter by stating what you want - reversal of the chargeback - and briefly restate why your evidence supports that outcome. This step is part of the broader chargeback representment process. Keep this section short. One or two sentences is enough. A clean closing conveys confidence and makes the letter feel complete instead of trailing off.

| Section | Purpose | Ideal Length |

|---|---|---|

| Opening Summary | State your position and the transaction details | 3-4 sentences |

| Factual Timeline | Walk through events in order with exact dates | 5-10 numbered points |

| Evidence References | Link each claim to a specific attached document | Woven into the timeline |

| Closing Request | Ask for the reversal and restate your strongest point | 1-2 sentences |

Common Mistakes That Tank an Otherwise Strong Rebuttal

Even merchants who follow a good structure can lose a chargeback dispute. The reasons are usually the same ones that come up again and again, and most of them have nothing to do with whether the transaction was legitimate.

The single fastest way to lose is to miss the deadline. Banks give you a fixed window to respond. If you submit even one day late, your rebuttal gets ignored entirely. Put the deadline in your calendar the moment you receive the dispute.

The next most common problem is submitting evidence that doesn't match the reason code. If the customer claimed they never received their order but you sent over a signed contract, that's not going to improve your case. Every piece of evidence you include should speak directly to the claim being made against you.

Emotional language is another pattern that shows up repeatedly - it's understandable to feel frustrated when a customer disputes a legitimate charge, but language like "this customer is lying" or "this is completely unfair" will hurt your credibility. Banks want facts and documentation, not feelings.

Higher-value transactions also face more scrutiny than smaller ones. Disputes over $300 have a win rate of just 27.64%, which reflects how much harder banks look at claims where more money is at stake. That means your evidence needs to be especially complete for bigger transactions - not just adequate. Merchants who accumulate too many disputes may also find themselves flagged as an excessive chargeback merchant, which adds another layer of consequences beyond individual losses.

A quick reference to keep you on track:

| Do This | Not This |

|---|---|

| Match your evidence to the reason code | Submit generic documents that don't address the claim |

| Stick to facts and a neutral tone | Use emotional or accusatory language |

| Submit before the deadline | Assume you have more time than you do |

| Include a clear timeline of events | Leave the bank to piece together the story themselves |

| Add extra documentation for high-value disputes | Treat all disputes as if they need the same level of proof |

One last thing worth mentioning: some merchants lose because they assume a strong case speaks for itself - it doesn't. A bank reviewer may spend only a few minutes on your submission, so you'll have to make the right conclusion easy to reach.

Your Chargeback Doesn't Have to Be a Done Deal

That edge matters more than ever right now. Dispute rates surged 78% year-over-year in Q3 2024, which means merchants who have not yet built a reliable rebuttal process are already falling behind. Knowing how to collect strong evidence, structure a persuasive argument, and stay away from the emotional missteps that undermine otherwise strong cases is fast becoming a core business skill - not just a back-office job.

The next step is simple: pull the chargeback case in front of you, find the reason code, and start building the response around the evidence that directly contradicts the claim. Losing by default is always optional. A well-written rebuttal letter is how merchants take that option off the table. If you want automated tools to help catch disputes earlier, learn more about how chargeback alerts work with Shopify stores.

Your Chargeback Doesn't Have to Be a Done Deal

That edge matters more than ever right now. Dispute rates surged 78% year-over-year in Q3 2024, which means merchants who have not yet built a reliable rebuttal process are already falling behind. The ability to collect strong evidence, structure a persuasive argument, and stay away from the emotional missteps that undermine otherwise strong cases is quickly becoming a core business skill - not just a back-office job.

The next step is simple: pull the chargeback case in front of you, find the reason code, and build the response around evidence that directly contradicts the claim. Losing by default is always optional. A well-written rebuttal letter is how merchants take that option off the table. If you're also weighing whether to issue a refund after a chargeback has already started, that decision deserves its own careful look before you respond.

FAQs

What do banks look for in a chargeback rebuttal letter?

Banks check rebuttals against a reason code and look for relevant, verifiable documentation. Vague statements don't work - independently checkable evidence like signed delivery confirmations or IP logs carries the most weight.

How long do I have to respond to a chargeback?

Most card networks give merchants between 7 and 11 days to respond once a chargeback is initiated. Missing this deadline means your rebuttal is ignored entirely, regardless of how strong your case is.

What evidence is strongest in a chargeback dispute?

Signed delivery confirmations and IP address or device logs are the strongest evidence types. Email threads and chat logs offer medium support, while order confirmations alone are considered weak evidence.

How should I structure a chargeback rebuttal letter?

Start with a factual summary, follow with a chronological timeline, reference each attached document by name, and close with a direct request for reversal. Keep every section concise and fact-based.

What mistakes most commonly cause merchants to lose chargebacks?

Missing the deadline, submitting evidence that doesn't match the reason code, and using emotional or accusatory language are the most common mistakes. High-value disputes over $300 also face significantly lower win rates and require extra documentation.