Call (844) NO-DISPUTES

Call (844) NO-DISPUTESWhat is a Credit Card Soft Descriptor?

A credit card soft descriptor is the temporary transaction label that appears on a cardholder's statement instantly after a purchase is made - it acts as a placeholder while the payment is still being processed, and what it says - or doesn't say - can make a lot of difference in how a customer perceives a charge.

For businesses, how soft descriptors work isn't just a technical detail - it can directly affect customer trust, dispute rates, and even revenue. Getting this small piece of text right can save you from unnecessary chargebacks and your customers from second-guessing every purchase they make with you.

How Soft Descriptors Show Up on Your Statement

When you make a purchase, your bank doesn't wait for the charge to completely process before showing something on your account - it shows a temporary label instantly. That label is the soft descriptor - it acts as a placeholder that appears during the authorization stage, before the payment is completely settled.

A way to imagine this is to buy something online and then check your banking app the next morning. You'll see the charge sitting in a pending state, and next to it will be a short line of text recognizing where it came from. That text is the soft descriptor doing its job.

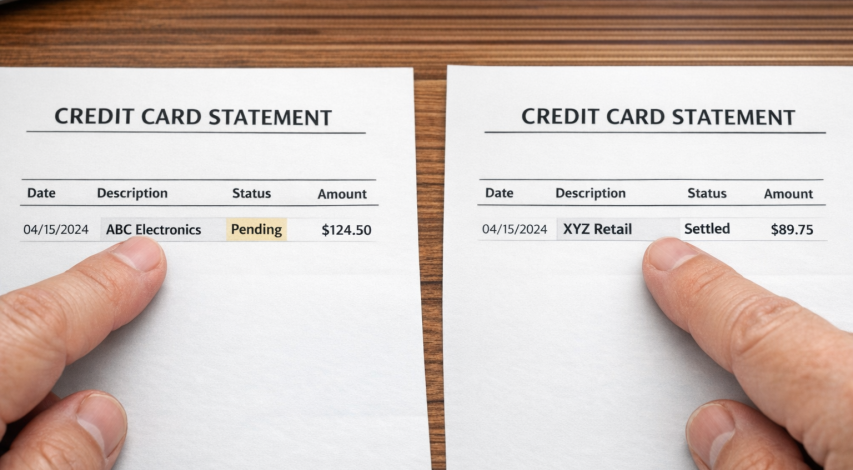

Once the transaction completely clears - usually within a few days - the soft descriptor can be replaced by what's called a hard descriptor. The hard descriptor is the final version that stays on your statement permanently. In a lot of cases the two look similar, but they don't always match, and that gap is where uncertainty starts for cardholders. You can read more about the difference between soft and hard descriptors if you want to understand how they compare.

The character limit for these labels is tight. Soft descriptors are usually capped between 20 and 25 characters, including spaces. That doesn't leave much room for a business to completely spell out its name or explain what the charge was for.

| Stage | Descriptor Type | Appears When |

|---|---|---|

| Authorization | Soft descriptor | Immediately after a transaction is initiated |

| Settlement | Hard descriptor | Once the charge is fully processed and posted |

A credit card soft descriptor is a short, temporary label attached to a pending charge - it exists so cardholders can see activity on their account in real time, even before the merchant has completely completed their side of the transaction.

Most never pay much attention to these labels until a charge looks unfamiliar; it's when the difference between a pending soft descriptor and a settled hard descriptor starts to matter quite a bit - and when it can sometimes lead to descriptor-related chargebacks if the cardholder doesn't recognize what they see.

Soft Descriptors vs. Hard Descriptors: What's the Difference

Every card transaction goes through two descriptor stages. The soft descriptor appears first, while the charge is still pending. Then, once the transaction settles, it gets replaced by a hard descriptor - the permanent version that stays on the statement.

Hard descriptors are set at the merchant account level and go through a formal registration process with the card networks. They are more stable and steady, and have less flexibility. Soft descriptors, in contrast, can be customized at the transaction level, which gives businesses a short window to show customers something more recognizable.

| Descriptor Type | When It Appears | How Long It Lasts | Character Limit |

|---|---|---|---|

| Soft Descriptor | When the charge is pending | Until the transaction settles | Up to 22 characters |

| Hard Descriptor | After the transaction settles | Permanently on the statement | Up to 22 characters |

The character limits are the same, but what fills those characters can look very different. A soft descriptor might show a product name or a website URL to help the customer find the charge. The hard descriptor is more likely to show the registered business name, which can be a legal entity name that customers don't instantly connect to the brand they shopped with.

That swap is where things get tough.

A customer might see a familiar name while the charge is pending, then see something different once it settles. They don't necessarily know that a swap happened - they just see a name that doesn't match what they expected. That's an actual gap that businesses can take steps to close, and one that can sometimes lead customers to file a credit card dispute.

One way to cut back on that uncertainty is to keep the soft and hard descriptors as consistent as possible. If your hard descriptor is a shortened legal name, try to make your soft descriptor something close to it, or at least something that connects back to the same brand. The goal is for a customer to find the charge at any point in the process - not just while it's pending.

Why Confusing Descriptors Trigger Disputes and Chargebacks

When a customer sees an unrecognizable charge on their statement, their first instinct is not to contact the business. Studies show that 76% of customers go straight to their bank to dispute a charge before they ever try to reach the merchant. That one detail explains quite a bit about how quickly a chargeback situation develops.

Chargebacks are not a minor inconvenience. Merchants lose the sale amount and also absorb chargeback fees, processing penalties, and in some cases, restrictions on their merchant account if dispute rates climb too high. The financial damage from a single confused customer can be a few times the value of the original transaction.

The numbers behind this are worth sitting with. Around 45% of all card disputes are linked to customers not recognizing a charge. That is not fraud, and it's not buyer's remorse - it's a non-fraud chargeback that failed to connect the charge to an actual purchase the customer made.

It gets harder to ignore when you realize that over 70% of customers find it easier to file a chargeback than to request a refund directly from a business. Merchants lose the chance to resolve things before they escalate, largely because the descriptor never gave the customer a reason to reach out.

There are a few common ways a descriptor ends up unrecognizable to customers.

A parent company name appears instead of the brand the customer actually bought from. An internal product code or abbreviation fills the descriptor field. The business name is truncated in a way that strips out the recognizable part. A third-party payment processor's name shows up instead of the merchant's. The descriptor includes no location, contact detail, or context that would help a customer place the charge.

None of these are unusual situations. They happen when descriptor fields are set up once and never revisited, or when businesses never check what actually appears on a customer's statement after a transaction goes through.

The core problem is a gap in recognition - a customer completes a purchase, then sees something on their statement that doesn't connect back to that memory. That gap is where disputes are born, and it costs merchants money that a better descriptor could have protected.

What Makes a Soft Descriptor Actually Work

A soft descriptor does its job when a customer reads it and instantly knows what the charge is for. That sounds simple, but businesses get it wrong by defaulting to a legal entity name or an internal shorthand that means nothing to the average person.

The most recognizable descriptors include a few important pieces of information. Your trading name or brand name should come first since that's what customers actually recognize. From there, you can add a product type or service category to give the charge more context. A short URL or customer service number is worth including too - it gives a direct way to get answers instead of going to their bank.

Character limits matter more than you know. Most U.S. processors cap descriptors at 25 characters, and that includes spaces. The sweet spot for readability is between 5 and 22 characters - short enough to display cleanly on a bank statement and long enough to say something helpful. Filling up to the limit with filler words is a waste of space.

| Do This | Not This |

|---|---|

| Use your recognizable brand name | Use a legal entity or parent company name |

| Add a product type or service label | Leave the descriptor as a generic code |

| Include a URL or phone number | Fill remaining characters with punctuation |

| Stay within 5-22 characters for clarity | Max out the limit without a reason to |

Dynamic descriptors take this a step further. Instead of one static name attached to every charge, a descriptor can change to match what was actually purchased. Most processors cap these at 20 to 25 characters as well, so the same rules apply - but the added specificity can make a real difference for businesses that sell across multiple product lines.

It is worth looking at your own descriptor with fresh eyes. If a customer saw that text on their statement with no other context, would they know it was you? Would they know what they bought? If the answer to either question is no, that's worth fixing - and if disputes do follow, understanding how chargebacks interact with partial refunds can save you from compounding the problem.

Your Descriptor Is Your First Line of Defense

Take a few minutes this week to audit where your business stands. A quick checklist to get started:

- Pull a recent statement and look at how your business name actually appears to cardholders - not how you set it up, but how it renders.

- Check for truncation by counting characters; aim to front-load the most recognizable part of your name.

- Include a phone number or URL in the descriptor so curious customers can reach you before they reach their bank.

- Contact your payment processor to confirm what you can control and request any necessary updates.

- Test across card networks - Visa and Mastercard can display descriptors differently, so verify both.

Most businesses never think about their soft descriptor until a chargeback forces them to - it takes less than an hour to review and fix, but it works in the background of every transaction you process. Few changes this small have this much potential to protect your revenue and your customer relationships.

FAQs

What is a credit card soft descriptor?

A soft descriptor is a temporary label that appears on a cardholder's statement immediately after a purchase, acting as a placeholder while the payment is still being processed and before it fully settles.

How is a soft descriptor different from a hard descriptor?

A soft descriptor appears while a charge is pending, while a hard descriptor is the permanent version that replaces it once the transaction fully settles. The two don't always match, which can confuse cardholders.

Why do confusing soft descriptors cause chargebacks?

When customers don't recognize a charge, 76% go straight to their bank to dispute it rather than contacting the merchant. Around 45% of all card disputes are linked to customers simply not recognizing a charge on their statement.

What should a good soft descriptor include?

A good soft descriptor should include your recognizable brand name, a product type or service label, and a short URL or customer service number so customers can identify the charge without filing a dispute.

How many characters can a soft descriptor contain?

Most U.S. processors cap soft descriptors at 25 characters including spaces. The recommended sweet spot for readability is between 5 and 22 characters to display cleanly while still conveying useful information.