Call (844) NO-DISPUTES

Call (844) NO-DISPUTESWhat is a Credit Card Settlement?

When debt becomes unmanageable, some start looking for a way out that goes past paying the minimum each month. One option that comes up is credit card settlement - a process where you negotiate with your creditor to pay back less than the full amount you owe. It sounds straightforward, and in some cases it legitimately can give you relief. But like most financial tools, it comes with tradeoffs that are worth knowing about.

I'm here to talk about what credit card settlement actually is, how the process works from start to finish, what it's likely to cost you - financially and otherwise - and what you should watch for along the way. The goal isn't to push you toward any particular choice, but to give you an honest picture so you can figure out if settlement makes sense for your situation.

Quick Answer

A credit card settlement is when a creditor agrees to accept less than the full amount owed to resolve a debt. This typically happens when an account is severely delinquent and the creditor believes collecting the full balance is unlikely. The debtor pays a lump sum or negotiated amount, and the remaining balance is forgiven. While it can eliminate debt for less than owed, settlements negatively impact your credit score and the forgiven amount may be considered taxable income by the IRS.

How Credit Card Settlement Actually Works

At its core, a credit card settlement is a negotiation between you and whoever you owe money to. That could be the original credit card company, or it could be a debt collection agency that bought your account. You want to agree on a lesser lump sum that closes out the debt entirely.

Creditors are more willing to negotiate once an account has gone a long time without payment. Once you're around 120 to 180 days past due, the creditor starts to see your debt as an actual loss. At that point, getting back a part of what you owe looks quite a bit better to them than nothing at all.

Most settlements land between 50% and 70% of the original balance. So if you owe $10,000, you might pay between $5,000 and $7,000 to completely resolve the account. That gap can make a genuine difference if you're working with limited funds.

The parties involved are usually just you and the creditor, though a third-party debt collector sometimes enters the picture. Credit card debt is frequently sold to collection agencies when the original lender decides to cut its losses. In that case, you'd be negotiating with the collector instead, and the process can change a little because they bought your debt at a discount. If you handle payments through a platform, it's also worth understanding what happens if Stripe closes your credit card processing during this time.

It's also worth knowing that the creditor has no obligation to accept less than you owe. Settlement only works because it's in their interest to recover something, and that calculation changes depending on your account history and how long the debt has been sitting there. Understanding the credit card dispute window can also matter if any charges are still being contested.

| Original Balance | Settlement at 50% | Settlement at 70% |

|---|---|---|

| $5,000 | $2,500 | $3,500 |

| $10,000 | $5,000 | $7,000 |

| $20,000 | $10,000 | $14,000 |

The numbers above are estimates, not guarantees, but they give you a basic sense of the range to expect.

The Step-by-Step Settlement Process

The process takes longer than expected and it doesn't move in a straight line. That said, there's a general sequence that most settlements follow.

- Stop making payments. Creditors generally won't negotiate with you while your account is in good standing. Payments need to stop before they'll consider a reduced amount.

- Save up a lump well sum. While your account falls behind, you'll want to set money aside. Most settlements get paid in one go, so you need a pool of cash ready before talks begin.

- Wait for the account to become delinquent. This usually takes several months. The creditor may sell the debt to a collections agency during this time, which changes who you'll be negotiating with.

- Contact the creditor or collector. Once the account is deep enough in arrears, you or a representative can reach out to start the conversation about settling.

- Negotiate the settlement amount. This back-and-forth can take time. The first number they give you is rarely the final one, so be prepared to push back.

- Get the agreement in writing. Before you hand over any money, ask for a written confirmation of the settlement terms. This protects you if there's ever a dispute later.

- Make the payment. Once you have written confirmation, send the agreed amount. Keep records of the payment as well.

You can go through this process on your own, or you can work with a debt settlement company to manage negotiations on your behalf. These businesses charge fees for their help, so it's worth understanding what you're paying for before you sign anything.

One thing to keep in mind: creditors don't have to say yes. They may counter with a higher number, ask for a payment plan instead of a lump sum, or simply decline. Patience is an actual part of this process - not just a great idea.

The timeline from first missed payment to final settlement can stretch anywhere from a few months to over a year. The length can depend on the creditor, the amount owed, and how quickly both sides can reach a number they'll accept. If you've ever wondered what happens when a dispute goes unanswered, the dynamics are surprisingly similar - delays and silence rarely help either side.

The Step-by-Step Settlement Process

The process takes longer than expected and it doesn't move in a straight line. That said, there's a general sequence that most settlements follow.

- Stop making payments. Creditors generally won't negotiate with you while your account is in good standing. Payments need to stop before they'll consider a reduced amount.

- Save up a lump sum. While your account falls behind, you'll want to set money aside. Most settlements get paid in one go, so you need a pool of cash ready before talks begin.

- Wait for the account to become delinquent. This usually takes several months. The creditor may sell the debt to a collections agency during this time, which changes who you'll be negotiating with.

- Contact the creditor or collector. Once the account is deep enough in arrears, you or a representative can reach out to start the conversation about settling.

- Negotiate the settlement amount. This back-and-forth can take time. The first number they give you is rarely the final one, so be prepared to push back.

- Get the agreement in writing. Before you hand over any money, ask for a written confirmation of the settlement terms. This protects you if there's ever a dispute later.

- Make the payment. Once you have written confirmation, send the agreed amount. Keep records of the payment as well.

You can go through this process on your own, or you can work with a debt settlement company to manage negotiations on your behalf. These businesses charge fees for their help, so it's worth understanding what you're paying for before you sign anything.

One thing to keep in mind: creditors don't have to say yes. They may counter with a higher number, ask for a payment plan instead of a lump sum, or simply decline. Patience is an actual part of this process - not just a great idea.

The timeline from first missed payment to final settlement can stretch anywhere from a few months to over a year. The length can depend on the creditor, the amount owed, and how quickly both sides can reach a number they'll accept. It's also worth understanding what happens if a creditor never responds to a dispute - the outcome can affect negotiations in unexpected ways.

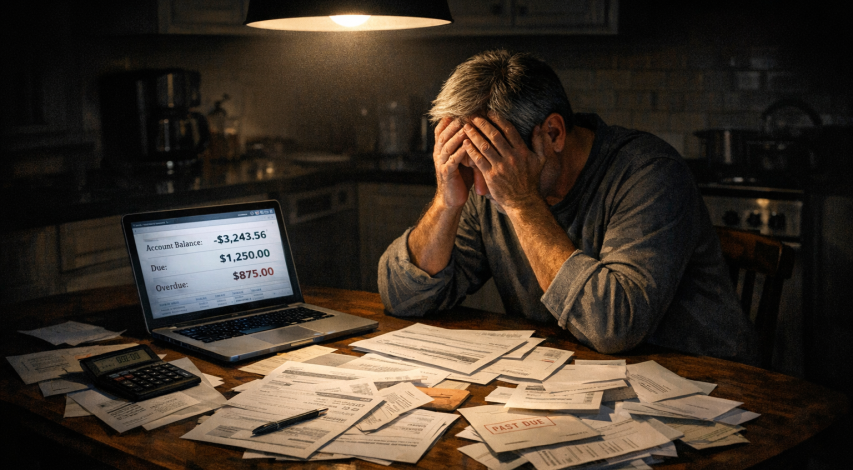

What Credit Card Settlement Costs You

Settlement can cut back on what you owe, but it comes with actual financial consequences that are worth considering. The savings on your balance don't tell the whole story.

The most immediate hit is to your credit score. To settle a debt, you usually have to stop making payments first - and each missed payment gets reported to the credit bureaus. By the time a settlement is reached, your credit history will show late payments, delinquencies, and a settled account instead of a paid one. That damage can stay on your credit report for as long as seven years.

If you use a settlement company to manage the process, their fees add even more cost. Most charge between 15% and 25% of your total enrolled debt, and that's on top of whatever you pay the creditor. So if you settle $20,000 in debt for $12,000, you could owe the settlement company anywhere from $3,000 to $5,000 on top of that.

There's also a tax consequence that a lot of people don't account for. The IRS treats forgiven debt as taxable income, and creditors are required to send you a 1099-C form for any forgiven amount over $600. That means you could owe income tax on the portion of debt that was wiped away.

It's helpful to try to see how settlement stacks up against other paths forward.

| Factor | Settlement | Minimum Payments | Debt Consolidation |

|---|---|---|---|

| Total Cost | Reduced balance + fees + possible taxes | Full balance + high interest | Full balance + lower interest |

| Credit Impact | Significant damage | Minimal if on time | Minor, short-term dip |

| Timeline | 2-4 years | Many years | 2-5 years |

| Tax Consequences | Yes, on forgiven amounts | No | No |

| Best For | Severe hardship, can't repay in full | Manageable debt load | Steady income, good enough credit |

Each path has trade-offs, and none of them are free. What matters is learning about the full cost of settlement - not just the number your creditor agrees to accept.

Red Flags and Risks Worth Knowing About

Settlement isn't just expensive in dollars - it can go sideways in ways that the cost overview alone doesn't capture. One of the biggest problems is the debt settlement industry itself. Some businesses in this space charge inflated fees, make promises they can't keep, and leave clients in worse shape than before.

Here are some warning signs worth watching for before you work with any settlement company.

- They ask for fees before settling any debt

- They guarantee a specific result or reduction amount

- They tell you to stop all communication with your creditors

- They pressure you to sign up quickly without reviewing your situation

- They can't clearly explain how their fees work

Legitimate help exists, but it pays to be careful about who you trust with something this important.

There's also a legal dimension that doesn't get talked about enough. Creditors can sue you to collect what you owe, and they don't always wait for you to come to the table first. The average amount mixed up in a credit card lawsuit is around $13,440 - and if a judgment is entered against you, the creditor may be able to garnish your wages or freeze a bank account. It's an actual outcome, not a worst-case scenario to dismiss.

Then there's the emotional side of the process. Settlement usually means months of not paying your accounts and fielding collection calls. That experience wears on you - it's not a passive process you can set and forget.

It's also worth saying directly: settlement isn't the right move for every situation. If your debt load is manageable and your income is stable, a debt management plan or a structured repayment strategy through a nonprofit credit counseling agency might get you to the finish line with less damage. Settlement makes the most sense when the debt is legitimately unmanageable and other paths have already been considered.

The point isn't to talk you out of anything - it's to make sure that the choice you land on is based on the full picture, not just the most desirable number a settlement company puts in front of you.

Is Credit Card Settlement Right for You?

Before making any decisions, take an honest look at your full financial picture. If you're not sure where to start, a nonprofit credit counseling agency can help you weigh your options - settlement, a debt management plan, or another path entirely - without the pressure of trying to sell you something. A well-educated strategy makes the difference.

Getting out of debt isn't quick or easy, but it is possible. Whatever path you choose, the most important step is choosing to take control. From there, everything else can become a little more manageable. If recurring charges are part of what got you here, understanding how credit card recurring billing works can help you spot and stop unwanted costs before they add up.

FAQs

What is a credit card settlement?

A credit card settlement is a negotiation where you agree to pay your creditor less than the full amount owed, typically resolving the debt entirely with a lump sum payment.

How much can you save through credit card settlement?

Most settlements land between 50% and 70% of the original balance. For example, a $10,000 debt could be settled for $5,000 to $7,000.

Does credit card settlement hurt your credit score?

Yes, significantly. Missed payments and settled accounts are reported to credit bureaus and can remain on your credit report for up to seven years.

Is forgiven debt from settlement taxable?

Yes. The IRS treats forgiven debt as taxable income. Creditors must send a 1099-C form for any forgiven amount over $600, meaning you may owe income tax on it.

When does credit card settlement make sense?

Settlement is best suited for situations where debt is genuinely unmanageable and other options like debt management plans or consolidation have already been considered and ruled out.